2024-05-15 06:55:00

GLOBAL OIL DEMAND +2.2 MBD

OPEC - May 14, 2024 - OPEC MONTHLY OIL MARKET REPORT

Oil Market Highlights

Crude Oil Price Movements

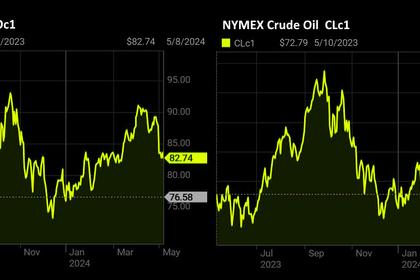

In April, the OPEC Reference Basket (ORB) value rose by $4.90, or 5.8%, m-o-m, to average $89.12/b. Oil futures prices averaged higher, with the ICE Brent front-month contract increasing by $4.33, or 5.1%, m-o-m to average $89.00/b, and the NYMEX WTI front-month contract rising by $3.98, or 4.9%, to average $84.39/b.

The DME Oman front-month contract rose by $5.12, or 6.1%, m-o-m, to average $89.37/b. The front-month ICE Brent/NYMEX WTI spread widened by 35¢ to average $4.61/b. The market structure of oil futures prices strengthened and money managers remained increasingly bullish about oil. The premium of light sweet to medium sour crudes narrowed across all major trading hubs on lower light distillate margins.

World Economy

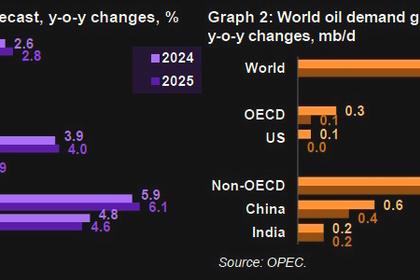

The world economic growth forecasts for 2024 and 2025 remain unchanged at 2.8% and 2.9%, respectively.

In the United States, economic growth for 2024 and 2025 are revised up slightly to 2.2% and 1.9%, respectively. The economic growth forecast for the Eurozone remains at 0.5% for 2024 and 1.2% for 2025. Japan’s economic growth forecast is also unchanged at 0.8% in 2024 and 1% in 2025. China’s economic growth forecast remains at 4.8% in 2024 and 4.6% in 2025. India’s economic growth forecast is unchanged at 6.6% for 2024 and 6.3% for 2025. Brazil’s economic growth forecast remains at 1.6% for 2024, and 1.9% for 2025. Russia’s economic growth for 2024 is revised up slightly to 2.3%, while the forecast for 2025 remains at 1.4%.

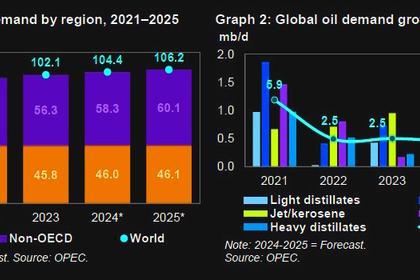

World Oil Demand

The global oil demand growth forecast for 2024 remains broadly unchanged from last month’s assessment at 2.2 mb/d. There were some minor upward adjustments to 1Q24 data, including a slight upward adjustment in OECD Americas and Chinese data due to better-than-expected performance in oil demand in 1Q24. However, this increase was offset by a downward revision to the Middle East in 2Q24 and 3Q24 due to an anticipated slight decline in these two quarters. Accordingly, the OECD is projected to expand by nearly 0.3 mb/d, while the non-OECD is forecast to grow by about 2.0 mb/d. Global oil demand growth in 2025 is expected to remain robust at 1.8 mb/d, y-o-y, unchanged from the previous month’s assessment. The OECD is expected to grow by 0.1 mb/d, y-o-y, while demand in the non-OECD is forecast to increase by 1.7 mb/d.

World Oil Supply

The non-DoC liquids supply (i.e. liquids supply from countries not participating in the Declaration of Cooperation) is expected to grow by 1.2 mb/d in 2024, unchanged from the previous month’s assessment. The main drivers for growth are expected to be the US, Canada, Brazil and Norway. In 2025, non-DoC liquids supply growth is expected at 1.1 mb/d, broadly unchanged from the previous month’s assessment. Again, growth is mainly driven by the US, Brazil, Canada and Norway.

Separately, DoC natural gas liquids (NGLs) and non-conventional liquids are forecast to grow by about 0.1 mb/d to average 8.3 mb/d in 2024, followed by a minor decline of about 10 tb/d to average 8.3 mb/d in 2025. The DoC crude oil production in April decreased by 246 tb/d, m-o-m, averaging 41.02 mb/d, as reported by available secondary sources.

Product Markets and Refining Operations

In April, refinery margins continued to trend downward as the recovery in refinery processing rates and stronger product output weighed on product markets. Most of the weakness stemmed from falling naphtha and diesel crack spreads due to slightly lower demand, which led to a lengthening balance for corresponding products, particularly in the Atlantic Basin. In Singapore, high middle distillate imports from India contributed to downward pressure on Southeast Asian refining profitability despite limited fuel oil crack spread gains and healthy regional gasoline requirements. Global refinery intake increased by 170 tb/d in April to average 80.0 mb/d compared with 79.8 mb/d in the previous month, but was 1.1 mb/d lower y-o-y.

Tanker Market

Dirty freight rates showed divergent trends in April. Very Large Crude Carrier (VLCC) spot freight rates were softer, with the Middle East-to-East route falling 11% m-o-m. In contrast, Suezmax spot freight rates improved, with the US Gulf Coast-to-Europe route seeing a 3% m-o-m increase. The Aframax market also improved, with intra-Med rates up 15%, although East of Suez rates declined. Rates for clean tankers declined on all reported routes, with East of Suez rates down 10% and West of Suez rates falling 20%.

Crude and Refined Products Trade

Preliminary data shows that US crude imports averaged 6.5 mb/d in April, representing an increase of 4%, m-o-m. US crude exports also moved higher, gaining 6% m-o-m to average 4.2 mb/d. US product imports rose by more than 3% to 6.5 mb/d in April, led by gains in gasoline inflows, while product exports were up by almost 3% supported mainly by outflows of propane/propylene, distillate fuel and jet fuel. The latest data for China shows crude imports continuing to climb, averaging 11.6 mb/d in March, representing an increase of 4%, m-o-m. Product imports into China jumped by over 26%, m-o-m, led by inflows of LPG and fuel oil, while product exports increased by around 33%, due to rising outflows of diesel oil, gasoline and jet fuel. India's crude imports in March recovered much of the previous month’s decline, averaging 4.9 mb/d for a gain of 8%.

India’s product imports fell 13% on lower inflows of LPG. In Japan, crude imports remained relatively flat in March, averaging 2.4 mb/d for a decline of 2%. Japan’s product exports increased by more than 18%, m-o-m, on support from most major products, except LPG. Preliminary estimates indicate OECD Europe crude imports remained relatively steady in April. Product imports into the region were slightly lower, amid a decline in jet fuel imports.

Commercial Stock Movements

Preliminary March 2024 data shows total OECD commercial oil stocks rose by 20.2 mb, m-o-m. At 2,793 mb, they were 121 mb below the 2015–2019 average. Within the components, crude and product stocks were up by 6.8 mb and 13.5 mb, m-o-m, respectively. OECD commercial crude stocks stood at 1,369 mb in March, which is 93 mb less than the 2015–2019 average. OECD total product stocks in March stood at 1,424 mb. This is 27 mb below the 2015–2019 average. In terms of days of forward cover, OECD commercial stocks increased in March by 0.2 days, m-o-m, to stand at 60.8 days. This is 1.7 days less than the 2015–2019 average.

Balance of Supply and Demand

Demand for DoC crude (i.e. crude from countries participating in the Declaration of Cooperation) remains unchanged from the previous month’s assessment to stand at about 43.2 mb/d in 2024, which is around 0.9 mb/d higher than the estimated level for 2023. Demand for DoC crude in 2025 remains unchanged from the previous month’s assessment to stand at 44.0 mb/d, around 0.8 mb/d higher than the level estimated for 2024.

-----

Earlier:

2024, May, 8, 07:00:00

OIL PRICE: BRENT BELOW $83, WTI ABOVE $78

Brent fell 30 cents, or 0.36%, to $82.86 a barrel, WTI fell 25 cents, or 0.32%, to $78.13 a barrel.

2024, May, 8, 06:55:00

RUSSIAN OIL REVENUE UP TWICE

Proceeds for the Russian budget from oil-related taxes jumped to 1.053 trillion rubles ($11.5 billion) last month compared to nearly 497 billion rubles in April 2023, according to Bloomberg calculations based on Finance Ministry data. Total oil and gas revenues in April increased nearly 90% year-on-year, to 1.23 trillion rubles, according to the data.

2024, May, 7, 07:00:00

OIL PRICE: BRENT BELOW $84, WTI NEAR $79

Brent were up 23 cents, or 0.28%, at $83.56 per barrel , WTI rose 24 cents, or 0.31%, to $78.72 a barrel.

2024, February, 16, 06:55:00

GLOBAL OIL DEMAND 2024: +2.2 MBD

The global oil demand growth forecast for 2024 remains unchanged from last month’s assessment at 2.2 mb/d.

2024, January, 22, 06:55:00

GLOBAL OIL DEMAND 2025: +1.8 MBD

The global oil demand growth forecast for 2024 remains unchanged at 2.2 mb/d, with the OECD growing by around 0.3 mb/d and the non-OECD by about 2.0 mb/d. The global oil demand growth in 2025 is expected to see a robust growth of 1.8 mb/d, y-o-y. The OECD is expected to grow by 0.1 mb/d, y-o-y, while demand in the non-OECD is forecast to increase by 1.7 mb/d.

2023, November, 22, 06:45:00

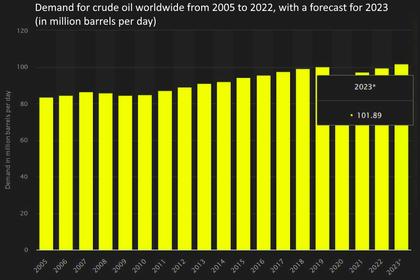

GLOBAL OIL DEMAND WILL UP BY 2.5 MBD

The world oil demand growth forecast for 2023 is revised up marginally from the previous month’s assessment to 2.5 mb/d.

2023, November, 17, 06:30:00

GLOBAL OIL DEMAND WILL UP

Global oil demand is now projected to rise by 2.4 million b/d in 2023 to 102 million b/d, but growth will decelerate to 930,000 b/d in 2024,