ACCELERATION OF THE ENERGY TRANSITION $5.7 TLN

IRENA - WORLD ENERGY TRANSITIONS OUTLOOK 2022

EXECUTIVE SUMMARY

IN 2022, THE NEED FOR THE ENERGY TRANSITION HAS BECOME EVEN MORE URGENT.

Given the inadequate pace and scope of the transition, anything short of radical and immediate action will diminish – possibly eliminate - the chance of staying on the 1.5°C or even 2°C path. In 2021, IRENA stressed the importance of a wide-ranging shift in the current trajectory across all energy uses. While some progress has been made, it falls woefully short of what is required. The stimulus and recovery efforts associated with the pandemic have also proved a missed opportunity, with only 6% of the G20’s1 USD 15 trillion in recovery funding in 2020 and 2021 being channelled towards clean energy (Nahm et al., 2022).

Acceleration of the energy transition is also essential for long-term energy security, price stability and national resilience. Some 80% of the global population lives in countries that are net energy importers. With the abundance of renewable potential yet to be harnessed, this percentage can be dramatically reduced. Such a profound shift would make countries less dependent on energy imports through diversified supply options and help decouple economies from wide swings in the prices of fossil fuels. This path would also create jobs, reduce poverty, and advance the cause of an inclusive and climate-safe global economy.

Overhauling the plans, policies, fiscal regimes and energy sector structures that impede progress is a political choice. With each passing day the cost of inaction pulls further ahead of the cost of action. Recent developments have demonstrated that high fossil fuel prices, in the absence of alternatives, result in energy poverty and loss of industrial competitiveness. But in the end, it is political will and resolve that will shape the transition path and determine whether it will lead to a more inclusive, equitable and stable world.

Towards the 2050 goal

IRENA’s 1.5°C pathway positions electrification and efficiency as key drivers of the energy transition, enabled by renewables, hydrogen, and sustainable biomass. This pathway, which requires a massive change in how societies produce and consume energy, would result in a cut of nearly 37 gigatonnes of annual CO2 emissions by 2050. These reductions can be achieved through 1) significant increases in generation and direct uses of renewables-based electricity; 2) substantial improvements in energy efficiency; 3) the electrification of end-use sectors (e.g. electric vehicles and heat pumps); 4) clean hydrogen and its derivatives; 5) bioenergy coupled with carbon capture and storage; and 6) last-mile use of carbon capture and storage.

Renewables-based electricity is now the cheapest power option in most regions. The global weighted-average levelised cost of electricity from newly commissioned utility-scale solar photovoltaic (PV) projects fell by 85% between 2010 and 2020. The corresponding cost reductions for concentrated solar power (CSP) were 68%; onshore wind, 56%; and offshore wind, 48%. As a result, renewables are already the default option for capacity additions in the power sector in almost all countries, and they dominate current investments. Solar and wind technologies have consolidated their dominance over time and, with the recent increase in fossil fuel prices, the economic outlook for renewable power is undeniably good.

Decarbonisation of end uses is the next frontier, with many solutions provided through electrification, green hydrogen and the direct use of renewables. Despite good global progress in deployment of renewables in the power sector, the end use sectors have lagged, with industrial processes and domestic heating still heavily reliant on fossil gas (see Table ES.1). In the transport sector, oil continues to dominate. In these sectors, deeper penetration of renewables, expanded electrification and improvements in energy efficiency can play a crucial role in alleviating concerns about prices and security of supply.

Despite some progress, the energy transition is far from being on track, and radical action is needed to change its current trajectory. Achieving the 2050 climate target depends on sufficient action by 2030, with the coming eight years being critical for accelerating the renewables-based transition. Any near-term shortfall in action will further reduce the chance of staying on path for the 1.5°C climate goal. Accelerated action is a no-regrets strategy and, when carefully implemented, allows the realisation of the benefits of a just and inclusive energy transition.

2030 priorities

This 2022 edition of the World Energy Transitions Outlook sets out priority areas and actions to reach the 2030 milestone using presently available solutions that can be deployed at scale. Progress will depend on political will, well-targeted investments, and a mix of technologies, accompanied by policy packages to put them in place and optimise their economic and social impact.

The top priorities are discussed below; they will have to be pursued simultaneously to put the energy transition on track to the 1.5°C goal.

Resolutely replacing coal power with clean alternatives, notably renewables, is vital. In recent months, gas scarcity and high prices have resulted in a slowdown of the global coal phase out, making an even stronger case for more aggressive deployment of renewables. It is evident that phase out is a complex task for countries heavily reliant on coal, especially given the imperative of a just and fair transition for affected workers and communities. Concerted action and international co-operation are therefore essential for timely progress. Replacing coal in industry must be tackled as well, as almost 30% of all coal is used in iron and steel, cement, and other industries. The coming years will be decisive for innovation, industry action, and international co-operation in these sectors.

Phasing out fossil fuels assets should be done in tandem with measures to eliminate market distortions and incentivise energy-transition solutions. This will involve phasing out fossil fuel subsidies and ensuring that the full costs (environmental, health and social) of burning fossil fuels are reflected in their prices, thereby eliminating existing market distortions. Fiscal policies, including carbon pricing, should be implemented and adjusted to enhance the competitiveness of transitionrelated solutions. Such interventions should be accompanied by a careful assessment of their social and equity impact, particularly on low-income populations, to ensure that they do not exacerbate energy poverty or have other socially regressive effects.

Ramping up renewables, together with an aggressive energy efficiency strategy, is the most realistic path towards halving emissions by 2030, as recommended by the IPCC.

In the power sector, renewables are faster and cheaper to deploy than the alternatives. But to meet the IPCC goal, annual additions of renewable power capacity will have to be three times the current rate of deployment. Such an increase is possible if the right conditions are in place. Technologyspecific targets and policies are especially needed to support less mature technologies, such as ocean energy and CSP.

Infrastructure upgrades, modernisation, and expansion are needed to increase system resilience and build flexibility for a diversified and interconnected system capable of accommodating high shares of variable renewable energy. The idea that fossil gas alone will be required to integrate higher shares of variable solar and wind is being fast overtaken by the improved economics of alternative sources of flexibility. But in addition to many technological solutions, markets will need to be adapted, both in liberalised and regulated systems. The current structure was developed during the fossil fuel era, to reduce operational costs of large, centralised power plants with differing fuel and opportunity costs. In the age of variable renewable energy, electricity should be procured considering the characteristics of decentralised generation technologies, with no fuel or opportunity cost.

Green hydrogen should move from niche to mainstream by 2030. In 2021, only 0.5 GW of electrolysers were installed; cumulative installed capacity needs to grow to some 350 GW by 2030. Hydrogen commands a great deal of policy attention, so the coming years should bring concrete actions to develop the global market and reduce costs. In this regard, the development of standards and guarantees of origin, along with support schemes to cover the cost gap for green solutions, will ensure that hydrogen offers a meaningful contribution to climate efforts in the long term.

Modern bioenergy’s contribution to meeting energy demand, including demand for feedstock, will have to triple by 2030. At the same time, the traditional use of biomass (such as firewood) needs to be replaced by clean cooking solutions. There is scope for biomass supply to expand, but the expansion will need to be managed carefully to ensure sustainability and minimise adverse outcomes. Policies that promote the wider use of bioenergy need to be coupled with strong, evidence-based sustainability procedures and regulations.

The majority of car sales by 2030 should be electric. Electromobility is a bright light of the energy transition progress, with EVs already at 8.3% of global car sales in 2021 (EV-Volumes, 2022). This share will rise rapidly in the coming years. Annual battery manufacturing capacity is set to quadruple between 2021 and 2025, to approximately 2 500 GWh. However, EV growth ultimately depends on a massive ramp-up of recharging infrastructure in the coming decade, as well as financial and fiscal incentives to promote the uptake of EVs, charger mandates, and bans on combustion engine vehicles. In addition, greater efforts should be made to reduce travel demand and to promote a switch to public transport and cycling where possible.

All new buildings must be energy efficient, and renovation rates should be significantly increased. Improving the measures and regulations for buildings can make an immense difference in the near term. Decarbonising heating and cooling will require changes to building codes, energy performance standards for appliances, and mandates for renewables-based heating and cooling technologies, including solar water heaters, renewables-based heat pumps and geothermal heating.

The effort to decarbonise heating and cooling will have to be sustained over the coming decades, but the measures just mentioned should be put in place without delay.

Demand-side management would help alleviate multiple challenges in the short term while contributing to the long-term security of energy and materials supply. Transforming the energy system is not simply about switching energy sources; it extends to ensuring the efficient use of energy across sectors. Innovation, recycling, and the circular economy will play significant roles in the pursuit of efficiency over the medium and long term. The coming years should see increased investment in research and development (R&D) and pilot projects along the value chains of all six of the technological avenues described above. This should be accompanied by efforts to cut unnecessary consumption and to move away from a system based on continuously increasing consumption.

Increasing ambition in national energy plans and in the Nationally Determined Contributions made under the 2015 Paris Climate Agreement must be firm enough to provide certainty of direction and guide investment strategies. The agreement on the Glasgow Climate Pact requested that parties revisit and strengthen the 2030 targets in their NDCs by the end of 2022 in line with the 1.5°C goal set out in the Paris Agreement. In addition to increasing ambition in their revised NDCs, Parties need to develop national implementation plans that include clearly defined targets, including efficiency, renewables and end uses.

A comprehensive set of policies covering all technological avenues is needed to achieve the necessary levels of deployment by 2030. Deployment policies should support market creation, thus facilitating reductions in technology costs and their scale up and increases in investment levels aligned with energy transition needs. Strong institutions will be needed to co-ordinate structural and just transition policies and manage potential misalignments. Only a holistic global policy framework can bring countries together to orchestrate a just transition that leaves no one behind and strengthens the international flow of finance, capacity and technologies.

IRENA’s socio-economic analysis shows that progressive policy and regulatory measures generate greater benefits from the energy transition. To gain insights about the impact of different policy baskets, a sensitivity analysis examines how the more ambitious energy transition pathway, 1.5°C Scenario, can result in different socio-economic outcomes depending on variations in international collaboration, carbon pricing, progressive fiscal measures and other government programmes (distributional policy).

The way forward

The 1.5°C Scenario will require investments of USD 5.7 trillion per year until 2030. Investment decisions are long-lived, and the risks of stranded assets are high, so decisions should be guided by long-term logic. IRENA estimates that USD 0.7 trillion in annual investments in fossil fuels should be redirected towards energy transition technologies. Measures to eliminate market distortions, coupled with incentives for energy transition solutions, will facilitate the necessary changes in funding structures. Most of the additional capital is expected to come from the private sector. But public financing will also have to double in order to catalyse private finance and create an enabling environment for speedy transition with optimal socio-economic outcomes.

By 2030, the 1.5°C-aligned energy transition promises the creation of close to 85 million additional energy transition-related jobs compared to 2019 and support a boost in global gross domestic product (GDP). The additional 26.5 million jobs in renewables and 58.3 million extra jobs in energy efficiency, power grids and flexibility, and hydrogen more than offset losses of 12 million jobs in the fossil fuel and nuclear industries. Meeting the human resource capacity necessary to fill these newly created jobs requires a scaling up of education and training programmes as well as measures aimed at building an inclusive and gender-balanced transition workforce. While global GDP is boosted under the 1.5°C pathway, the analysis presented in this report reveals that regionaland country-level variances will depend highly on policy and regulatory measures and international co-operative flows of financial assistance and knowledge.

The largest energy consumers and carbon emitters will have to implement the most ambitious plans and investments by 2030. This will require going beyond long-term decarbonisation commitments and setting out concrete operational targets, plans and policies for the short and medium term. G20 and G7 countries have a critical role in leading the global energy transition effort at the international level. Funds and knowledge must be made available to less wealthy nations to advance the quest for an inclusive and more equitable world.

Globally and in most countries, higher socio-economic benefits are obtained under the 1.5°C pathway than under the business-as-usual scenario. To support these positive outcomes, however, progressive policies and programmes will be essential. As analysed in this report, their key impact is the significant improvement in the distribution of the socio-economic benefits of the transition across societies and geographies.

IRENA’s Energy Transition Welfare Index shows that the 1.5°C pathway improves global welfare significantly. The Index, with its five dimensions,2 provides a holistic vision of the transition’s socioeconomic impacts. The following insights deserve particular attention:

• Assessing the impact of policies on the socio-economic footprints of transition roadmaps conveys a better understanding of the lived experience of the transition. Policy makers should explore these impacts and adjust their plans to ensure maximum shared benefits of climate policies.

• Implementing more progressive fiscal and regulatory measures and programmes, both domestically and internationally, will temper the regressive impacts of carbon taxes while improving the distribution of transition benefits and burdens.

• Enabling a rapid transition that complies with climate goals requires political commitment to support higher levels of international co-operation. By 2030, international climate collaboration should dramatically increase from current levels. Introducing these higher levels of international co-operation and more progressive distributional policies will ensure a fair and just transition.

Achieving universal access to modern energy by 2030 is a vital pillar of a just and inclusive energy transition aligned with the 1.5°C goal. Despite advances, the universal energy access goals of United Nations Sustainable Development Goal 7 are in jeopardy. An estimated 758 million people were living without electricity globally in 2019; 2.6 billion had no access to clean cooking fuels and technologies. On the current trajectory, the world is set to miss the target of universal access by a wide margin. Decentralised renewable energy solutions can play a crucial role in solving the access problem while supporting the delivery of essential services and income-generating activities across sectors.

The year 2022 is presenting new challenges, with concerns about rapidly rising energy prices and energy security. At the same time, the 1.5°C climate goal is slipping farther out of reach; short of dramatic and immediate action, it will slip away for good. This edition of the World Energy Transitions Outlook sets out how both agendas can be addressed through an accelerated energy transition, with the deployment of renewables scaled up across sectors. The business case for more renewables is becoming stronger, and the benefits will be wide-ranging. But clear plans and strategies are needed.

The time to act is now. The rest of the decade to 2030 is a critical milestone to ensure that 1.5°C remains a viable target for 2050.

-----

Earlier:

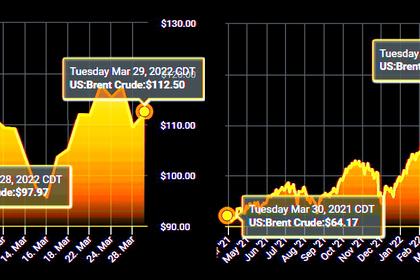

2022, March, 29, 13:30:00

GLOBAL ENERGY, COMMODITY CRISIS

The sanctions against Russia are the hardest we have seen against any country to date and in particular the decision to freeze $600bn of Russian foreign reserves is a first, which will have huge consequences in the long-term.

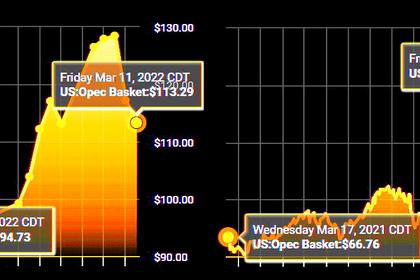

2022, March, 16, 12:15:00

GLOBAL OIL DEMAND 2022: +4.2 MBD

The 2022 forecast for global oil demand growth remains under assessment at 4.2 mb/d, with OECD forecast at 1.9 mb/d and non-OECD at 2.3 mb/d.

2022, February, 23, 12:30:00

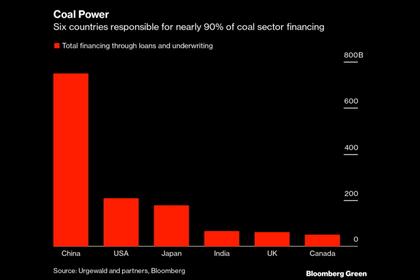

GLOBAL COAL INVESTMENT $1.5 TLN

The world coal industry has secured $363 billion in bank credits in the period from January 2019 to November 2021, and banks continued to support transactions on the sale of securities of companies in the industry, with their combined sum totalling $1.2 trillion.

2022, February, 21, 11:50:00

GLOBAL ENERGY CRISIS & STABILISATION

In the situation that has obtained in recent months on energy markets, it has become clear that one of the foundations of stability of the modern global world is, in the first instance, reliable energy supply, which cannot be provided without observing a reasonable balance of energy sources and an absence of discrimination against traditional sectors of the fuel and energy complex.

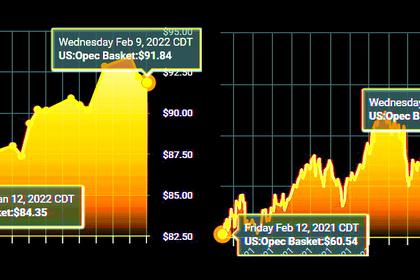

2022, February, 11, 11:40:00

GLOBAL OIL DEMAND 2022: +4.2 MBD

In 2022, oil demand growth is expected at 4.2 mb/d unchanged from last month, with OECD and non-OECD projected to grow by 1.8 mb/d and 2.3 mb/d, respectively.

2022, January, 17, 11:45:00

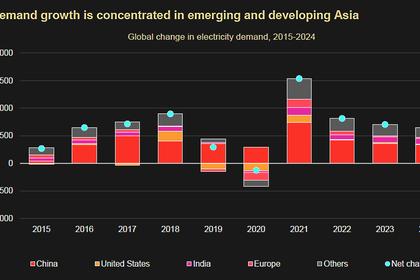

GLOBAL ELECTRICITY DEMAND UP BY 6%, 1 500 TWH

After small drop in 2020, global electricity demand grew by 6% in 2021. It was the largest ever annual increase in absolute terms (over 1 500 TWh) and the largest percentage rise since 2010 after the financial crisis.

2022, January, 12, 10:25:00

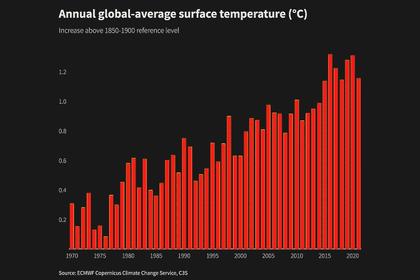

GLOBAL CLIMATE 2021: THE HOTTEST

The EU's Copernicus Climate Change Service (C3S) said in a report on Monday that the last seven years were the world's warmest "by a clear margin" in records dating back to 1850 and the average global temperature in 2021 was 1.1-1.2C above 1850-1900 levels.