RENEWABLE ENERGY NEEDS INVESTMENTS

IRENA - GLOBAL LANDSCAPE OF RENEWABLE ENERGY FINANCE 2020

EXECUTIVE SUMMARY

Global investment in renewable energy made significant progress between 2013 and 2018, with a cumulative USD 1.8 trillion invested. The decrease in installation costs, resulting from improvements in technology and the adaptation of procurement mechanisms to changing market conditions, has proven to be an effective catalyst in ramping up investment and building additional capacity.

This second edition of the Global Landscape of Renewable Energy Finance presents key global investment trends between 2013 and 2018 by region and sector, maps the role of different financial instruments and explores key differences between private and public actors. While the landscape is encouraging at first sight, the data suggest that the international community still has a long way to go to reach the level of investment necessary to achieve international climate and development goals.

The analysis also paints an unequal picture of the landscape of renewable energy finance, skewed heavily toward private actors operating in a handful of key countries. While investment has held a steady course in China, the United States and Western Europe, regions such as Latin America and the Caribbean, South Asia, and Sub-Saharan Africa remain under-represented in current global renewable energy investments.

For the first time, this report also looks at financial commitments to off-grid renewable energy technologies, which present a compelling costeffective answer to the challenge of ensuring universal access to sustainable energy, especially for populations and businesses in rural areas.

The in-depth analysis of off-grid renewable energy investments presented here offers a distinct perspective on the ever-increasing role of renewable energy in the energy access space.

Following the outbreak of the coronavirus (COVID-19), renewable energy investments saw a 34% decline in the first half of 2020, compared with the same period in 2019 (BNEF, 2020a). Going forward, there is a risk that the impacts of the global crisis on both the energy and financial sectors may negatively affect renewable energy investment, hampering progress toward a global energy transition. Nevertheless, the current pandemic seems to have increased investors' interest in more sustainable assets, such as renewables, as these have proven more resilient than conventional assets to the volatility caused by the COVID-19 crisis. By placing renewables at the core of their green stimulus packages, governments can signal long-term public commitment to the industry, boosting investor confidence and attracting additional private capital to the sector (IRENA, 2020a).

Emerging trends and global overview

Investment in renewable energy continued its steady increase from 2013 levels, peaking at USD 351 billion in 2017 before decreasing to USD 322 billion in 2018. This slowdown in global investment level masks the fact that falling technology costs allowed for more generation capacity installed for each dollar invested.

Together with favourable investment in previous years, 2018 ended with an increase in installed renewable generation capacity, with combined solar photovoltaic (PV) and wind (onshore and offshore) capacity additions equal to 149 gigawatts (GW), 6% higher than in 2017. Increased economies of scale, manufacturing and technology improvements, greater competition in supply chains, support for research and development, and direct deployment policies (e.g., auctions and feed-in tariffs) that have supported the uptake and increased maturity of renewable energy contributed to a 12% decrease in the levelised costs of electricity for solar PV and 14% for onshore wind between 2017 and 2018 (IRENA, 2019a).

While trends in investments, capacity additions and levelised costs all suggest encouraging progress in the renewable energy sector, renewable energy investment still falls short of what would be needed to put the world on a pathway compatible with keeping the rise in global temperatures to well below 2 degree Celsius (°C) and toward 1.5°C in this century (IRENA, 2020b). Annual investment in renewables would need to almost triple from an average of just below USD 300 billion in 2013-2018 to almost USD 800 billion through 2050. Further investments will be required in system integration technologies such as distributed energy resources, batteries and energy storage to enable the integration of new capacity additions into energy systems.

While it is necessary to scale up renewable energy investment, that in itself is not enough. A scale-up of renewable energy investment must be coupled with a significant reduction and redirection of fossil fuel investments. Although investments in renewable energy in the power sector exceeded those in fossil fuels, overall fossil fuel investments (i.e., including investments for infrastructure) far exceeded those in renewables. In 2018, renewables received USD 322 billion, mostly in the power sector, whereas investments in the fossil fuel sector amounted to USD 933 billion, of which USD 127 billion was for power generation.

Investment by technology

In 2017 and 2018, solar PV and onshore wind consolidated their dominance in the renewable energy market, representing on average 77% of total finance commitments in renewable energy (Figure ES.1). The highly modular nature of these technologies, their short project development lead times, increasing competitiveness driven by technology and manufacturing improvements, and appropriate policies and measures play an important role in explaining these technologies' large share of global renewable energy investment. Investment in offshore wind has picked up, attracting, on average, USD 21 billion a year globally between 2013 and 2018, and representing 8% of the total renewable capacity addition in 2018. According to IRENA (2020b), offshore wind holds considerable growth potential and will have a key role to play in achieving a level of deployment to support a decarbonised growth trajectory.

Investment by region

The East Asia and Pacific region attracted, on average, 32% of global renewable energy financial commitments in 2017-2018, peaking at USD 125 billion in 2017. This was mainly driven by increased spending on solar PV and onshore and offshore wind in China, which represented, on average, 93% of renewable energy investment in the region between 2013 and 2018.

Continued investment growth in the United States represented a significant boost to investment in member countries of the Organisation for Economic Co-operation and Development (OECD) located in the Americas. Together, these constituted the second destination for commitments in 2017-2018, attracting 22% of global investments in renewable energy, with a USD 82 billion peak in 2018.

Western Europe continued to be one of the main destinations for renewable energy investment, receiving, on average, USD 51 billion in 2017-2018, or 15% of total investment in the sector. In contrast, investment in OECD countries in Asia dropped in 2017-2018, down 53% compared to 2015-2016 levels, partly due to a decrease in solar PV investments in Japan.

Countries in Central Asia, Eastern Europe, Latin America and the Caribbean, Middle East and North Africa, South Asia and Sub-Saharan Africa collectively attracted, on average, only 15% of total renewable energy investment between 2013 and 2018, or USD 45 billion.

Financial instruments

Renewable energy projects are financed mainly with project-level conventional (i.e., nonconcessional) debt, which peaked at USD 119 billion in 2017 and accounted for 32% of the total investment in 2017-2018, on average. Balance sheet financing, both equity and debt, also supported considerable investment, each contributing to 27% (or 54% combined) of total commitments in 2017-2018, on average. Balance sheet financing was almost exclusively used to finance the development of solar PV and onshore wind, whereas project-level conventional debt was used for a wider range of technologies, including offshore wind.

Green bonds have the potential to channel significant volumes of capital into renewable energy. Annual issuance of green bonds solely earmarked to renewable energy experienced a rapid increase in recent years, from USD 2 billion in 2013 to USD 38 billion in 2019. Often used to re-finance existing assets, green bonds can attract institutional investors due to their large ticket sizes.

Public and private finance

Private finance provided, on average, 86% of total investment for renewable energy projects between 2013 and 2018, equivalent to annual commitments of USD 257 billion. Public finance reached an average of USD 44 billion annually in the same period.

Throughout 2013-2018, project developers continued to be the main actors within private finance, providing an average of 56% of total private finance in 2017-2018, mainly through balance sheet finance, either through debt or equity (Figure ES.2).

Commercial banks and investment banks represented, on average, 25% of total private finance in 2017-2018, often providing nonconcessional debt to mature technologies such as solar PV and onshore wind, as well as offshore wind. Institutional investors (including pension plans, insurance companies, sovereign wealth funds, endowments and foundations), provided, on average, only 2% of private direct investment in new renewable energy projects in 2017-2018.

The role of non-energy-producing corporations in renewable energy has gained attention in recent years, accounting, on average, for 6% of private finance in 2017-2018.6 Renewable energy investments from non-energy-producing companies are mainly motivated by the costsaving potential resulting from increasingly price-competitive renewable technologies, longterm price stability and security of supply, in addition to social and environmental concerns.

Corporate actors have a significant role to play in decarbonising the energy sector as they account for about two-thirds of the world's energy consumption (IRENA, 2018a).

Public finance, which provided on average 14% of total investments between 2013 and 2018, saw a peak in 2017 with 19%, due to a spike in investment from national development finance institutions (DFIs) in China, Colombia, Mexico and Turkey. National, bilateral and multilateral DFIs have consistently provided the majority of public investment, committing on average USD 37 billion annually between 2013 and 2018. Governments directly provided, on average, 9% of public finance in 2017-2018, up from 5% in 2015-2016, most of which was directed to solar PV and onshore wind projects.

Public finance has a key role to play in providing capital to technologies and regions that still require additional support to reduce the cost of capital, e.g., through the provision of risk mitigation instruments. The public sector can also reduce technology costs by demonstrating the business potential of hard-to-enter sectors and markets, such as off-grid renewables in rural areas.

Off-grid renewable energy investment trends The world is currently not on track to achieve universal energy access by 2030. As of 2018, approximately 789 million people had no access to electricity, and nearly 620 million people are estimated to remain in this situation until 2030 under current and planned policies (IEA, IRENA, UN, WBG, and WHO, 2020). Decentralised renewable energy can be a cost-effective solution to enable electrification, especially in rural areas where grid expansion may not be viable.

Between 2007 and 2019, off-grid renewables attracted about USD 2 billion of cumulative investment, USD 734 million of which was directed to energy-access-deficit countries that are home to 80% of the world population lacking adequate access to energy.

Annual financial commitments to decentralised renewables increased from USD 250 000 in 2007 to USD 460 million in 2019. Despite this growth, investments in off-grid renewable energy solutions still represent a very small portion of the overall financing for energy access – less than 1% of the total energy access investments in access-deficit countries.

Recommendations and conclusion

Meeting international climate objectives, as set by the Paris Agreement, will require an accelerated transformation of the global energy system, encompassing not only renewable energy, but also renewable energy systems integration and enabling technologies, energy efficiency measures and the increased electrification of end-uses (e.g., heating and transport) with renewables-based power. Most importantly, it will require a phase-out of investments into fossil fuels.

The combined efforts of a variety of stakeholders, including policy makers, capital market players, issuers and investors, are needed to shift investments away from fossil fuels and activate all available sources of capital in the renewable energy industry.

1. Use public finance to crowd in private capital

The private sector has dominated renewable energy investments in recent years and will likely fill in most of the financing gap. Nonetheless, limited public resources are key to closing the gap.

Public finance should be used strategically with the purpose of crowding in additional private capital, particularly in more difficult sectors and regions.

This can, for example, be achieved through capacity building, support for pilot projects and innovative financing instruments, blended finance initiatives and the provision of risk mitigation instruments (e.g., guarantees, currency hedging instruments and liquidity reserve facilities).

2. Mobilise institutional investment in renewables

With about USD 87 trillion of assets under management, institutional investors have a key role to play in reaching the investment levels required for the ongoing global energy transition. Greater participation of institutional capital will require a combination of effective policies and regulations, capital market solutions that address the needs of this investor class (e.g., green bonds), as well as a variety of internal changes and capacity building on the part of institutional investors (IRENA, 2020d).

3. Promote greater use of green bonds for renewables

Green bonds can help attract institutional investors and channel considerable additional private capital in the renewable energy sector to contribute to filling the significant outstanding investment gap.

Some recommended actions for policy makers and public finance providers to further increase green bond issuances include the adoption of green bonds standards in line with international climate objectives, the provision of technical assistance and economic incentives for green bond market development, and the creation of bankable project pipelines (IRENA, 2020e).

4. Enhance the participation of corporate actors

Although companies that produce renewable energy are already providing substantial investment in the sector, non-energy-producing corporations have a preeminent role to play in the energy transition by driving demand for renewable energy. By setting up the right enabling framework, policy makers can encourage active corporate sourcing and unlock additional capital in the sector. Recommended actions include, for example, establishing a transparent system for the certification and tracking of renewable energy attribute certificates, enabling third-party sales between companies and independent power producers, and creating incentives for utilities to provide green procurement options for companies (IRENA, 2018a).

5. Scale up financing for off-grid renewables

Annual investment of USD 45 billion in modern energy is required to achieve universal access by 2030 (IEA, IRENA, UN, WBG, and WHO, 2020).

Lack of access to affordable finance remains one of the biggest challenges for off-grid renewable energy projects, both upstream for project developers and downstream for energy users. New financing approaches (e.g., results-based financing) and tools (standardisation of project documentation and aggregation) are therefore needed to ensure improved access to capital and to reach the scale of investment needed to achieve universal energy access by 2030.

-----

Earlier:

2020, November, 10, 11:00:00

CLEAN AND RELIABLE ENERGY

It’s possible that the coming transportation revolution will greatly reduce demand on the grid.

2020, November, 6, 12:25:00

IBERDROLA RENEWABLE INVESTMENT $88 BLN

Pursuing the opportunities created by the “energy revolution” facing the world’s major economies should help to boost net profit by more than 40% from 2019 to 5 billion euros in 2025, Iberdrola said.

2020, November, 5, 12:20:00

CLEAN ENERGY INVESTMENT $2 TLN

Increasing annual investment to $2 trillion per annum between 2021 and 2023 will encourage more private sector investment, providing an effective stimulus for the global economy.

2020, November, 3, 13:00:00

RENEWABLE ENERGY FOR UAE

Strategic planning for a sustainable future Renewable energy is an essential requirement for sustainability and stands at the forefront of the UAE’s strategic priorities.

2020, November, 2, 17:00:00

HYDROGEN FOR DECARBONIZATION

While burning hydrogen is a carbon neutral activity and impacts Scope 3 emissions positively, the hydrogen itself may not be produced in a carbon neutral application.

2020, October, 29, 16:45:00

RENEWABLE VIRTUAL POWER PLANTS

Virtual Power Plant technologies are changing the way the electricity grid interacts with Renewable and Distributed Energy Resources.

2020, October, 12, 11:30:00

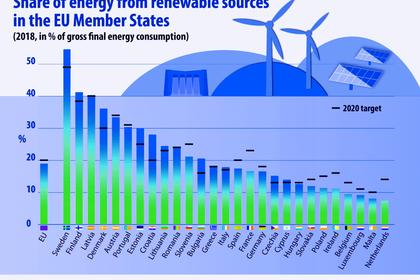

RENEWABLES FOR EUROPE

The demand for renewable energy documented with Guarantees of Origin shows record growth during the first half of 2020, despite the negative effect COVID-19 is having on global and local economies.