Analysis

2020, October, 29, 17:00:00

NORWAY'S OIL & GAS PRODUCTION 1.722 MBD ANEW

Preliminary production figures for September 2020 show an average daily production of 1 772 000 barrels of oil, NGL and condensate.

2020, October, 29, 16:35:00

TC ENERGY NET INCOME $904 MLN

TC Energy Corporation (TSX, NYSE: TRP) (TC Energy or the Company) today announced net income attributable to common shares for third quarter 2020 of $904 million

2020, October, 29, 16:30:00

SHELL INCOME $489 MLN

Income attributable to Royal Dutch Shell plc shareholders was $0.5 billion for the third quarter 2020

2020, October, 29, 16:25:00

NOVATEK PROFIT RUB13.2 BLN

Profit attributable to shareholders of PAO NOVATEK amounted to RR 13.2 billion

2020, October, 28, 14:15:00

OIL PRICE: NEAR $40

Brent were down $1.20, or 2.9%, at $40 a barrel, WTI was down $1.49, or 3.7%, at $38.08.

2020, October, 28, 14:10:00

INDIA'S LNG DEMAND UP

With coal delivering to India for less than $3/MMBtu, the price is still more competitive than LNG,

2020, October, 28, 14:05:00

EXXON LNG FOR ASIA

ExxonMobil predicts that, by 2030, China’s LNG imports will “probably exceed” 90mn t/yr—50pc growth even from 2019.

2020, October, 28, 14:00:00

EXXON LNG FOR INDIA

With India’s growing gas demand outstripping domestic production, LNG is playing an increasingly important role.

2020, October, 28, 13:50:00

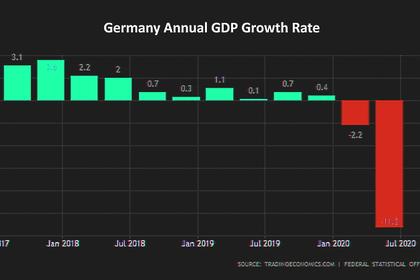

GERMAN ECONOMY UP 6%

The German economy likely grew by around 6% in the third quarter

2020, October, 27, 14:50:22

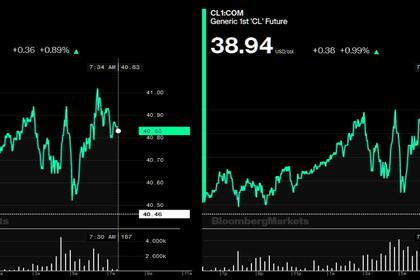

OIL PRICE: NEAR $41 ANEW

Brent was up 52 cents, or 1.3%, at $40.98 a barrel, WTI gained 38 cents, or 1%, to $38.94.

2020, October, 27, 14:45:00

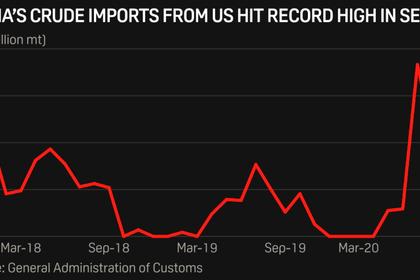

CHINA OIL IMPORTS UP

Crude oil is considered a key product to complete China's annual energy purchase commitments due to the commodity's typically higher value and volume compared with other energy products.

2020, October, 27, 14:40:00

INDIA GAS CONSUMPTION UP

Gas accounts for little over 6pc of India’s primary energy consumption mix, which is far below the global average. New Delhi has set a target to raise this to 15pc by 2030,

2020, October, 27, 14:30:00

U.S. LNG FOR INDIA

The US was the fifth-largest supplier of LNG to India in 2019, according to the Department of Energy.

2020, October, 27, 14:25:00

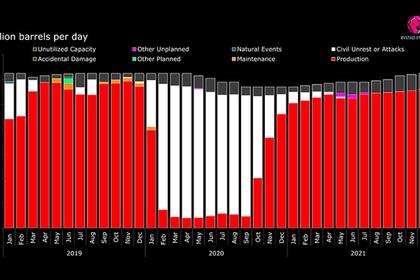

LIBYAN OIL RECOVERY

Libya's crude and condensate output has more than quintupled over the past month, averaging just close to 600,000 b/d on Oct. 26 as more oil fields in the southwest and southeast have restarted operations, sources added.

2020, October, 27, 14:05:00

NOV VARCO NET LOSS $55 MLN

National Oilwell Varco, Inc. (NYSE: NOV) today reported third quarter 2020 revenues of $1.38 billion, a decrease of seven percent compared to the second quarter of 2020 and a decrease of 35 percent compared to the third quarter of 2019.